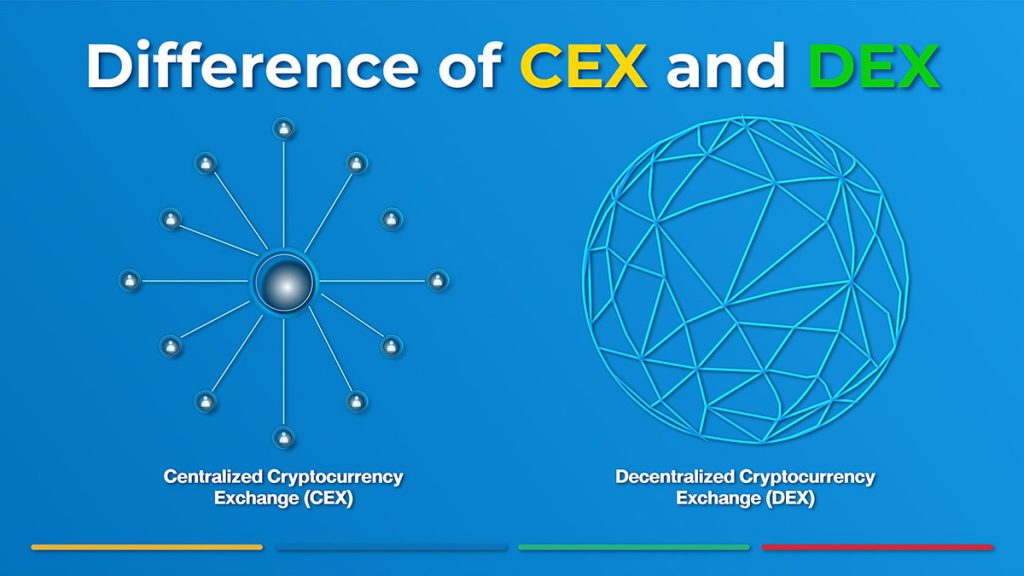

ContributionDAO Joins SIX Protocol as a Node Validator

SIX Network Expands Collaboration with ContributionDAO to Strengthen SIX Protocol Through Node Validator Participation SIX Network expands its collaboration with

Why SIX Network Is Building Infrastructure for RWA

SIX Network continues to develop RWA infrastructure so that when people talk about RWA, they think of the real-world use

How the Partnership Opens a New Direction for RWA Infrastructure at SIX Network

Following the announcement of our partnership with Piggycell, a South Korea-based RWA Infrastructure company in the energy sector, many may

SIX Network ประกาศความร่วมมือเชิงกลยุทธ์กับ Piggycell เพื่อร่วมผลักดัน RWA ระหว่างไทยและเกาหลีใต้

SIX Network ประกาศความร่วมมือเชิงกลยุทธ์กับ Piggycell บริษัทจากเกาหลีใต้ที่พัฒนาโครงสร้างพื้นฐาน Real-World Asset สำหรับพลังงานเคลื่อนที่ ภายใต้แนวคิด RWA Infrastructure for Mobile โดย Piggycell นำพลังงานในโลกจริง มาเชื่อมต่อกับระบบ Web3 ผ่าน DePIN

SIX Network Announces Strategic Partnership with Piggycell to Advance RWA Between Thailand and South Korea

SIX Network announces a strategic partnership with Piggycell, a South Korea-based company developing Real-World Asset infrastructure for mobile energy under

Tokenization Signals: Why RWA Is the Trend of This Year

Welcome to the Tokenization Signals series, an update on signals and growth in the RWA market, and what SIX is